Decoding AARP Plan F Premiums Across the US

Medicare can be a labyrinth, and choosing the right supplement plan can feel like navigating it blindfolded. But what if you could decode the costs, understand the nuances of AARP Plan F premiums by state, and make an empowered decision about your healthcare future? This comprehensive guide dives deep into the intricacies of AARP Plan F, providing a clear roadmap to help you find your way.

AARP Plan F, renowned for its comprehensive coverage, has long been a popular choice for those seeking robust Medicare supplementation. However, the landscape of Plan F premiums varies significantly across state lines. Understanding these variations, the factors that drive them, and how to find the best value for your specific location is crucial for maximizing your healthcare investment. This exploration aims to equip you with the knowledge to navigate these complexities and make informed choices.

AARP, a respected advocacy group for individuals aged 50 and over, partners with UnitedHealthcare to offer Medicare Supplement plans, including Plan F. These plans are designed to fill the gaps in Original Medicare coverage, offering additional financial protection against out-of-pocket expenses. The cost of these plans, specifically Plan F premiums, are subject to various regulatory and market-driven influences that differ from state to state.

One of the primary drivers of premium variations is the state's regulatory environment concerning Medicare Supplement plans. Some states implement stricter regulations on pricing and benefits, impacting the premiums offered by insurers. Additionally, the cost of healthcare services within a state can influence Plan F premiums. Regions with higher healthcare costs typically see higher premiums for supplemental plans.

Furthermore, competition among insurers plays a significant role in shaping premium landscapes. States with a greater number of insurance providers offering Plan F often see more competitive pricing. Understanding the interplay of these factors is paramount in your search for the optimal AARP Plan F coverage.

Historically, Plan F was a go-to choice for comprehensive coverage. However, changes in Medicare regulations have made Plan F less available to new Medicare beneficiaries. Those who already had Plan F can keep it, but understanding its evolving landscape is critical.

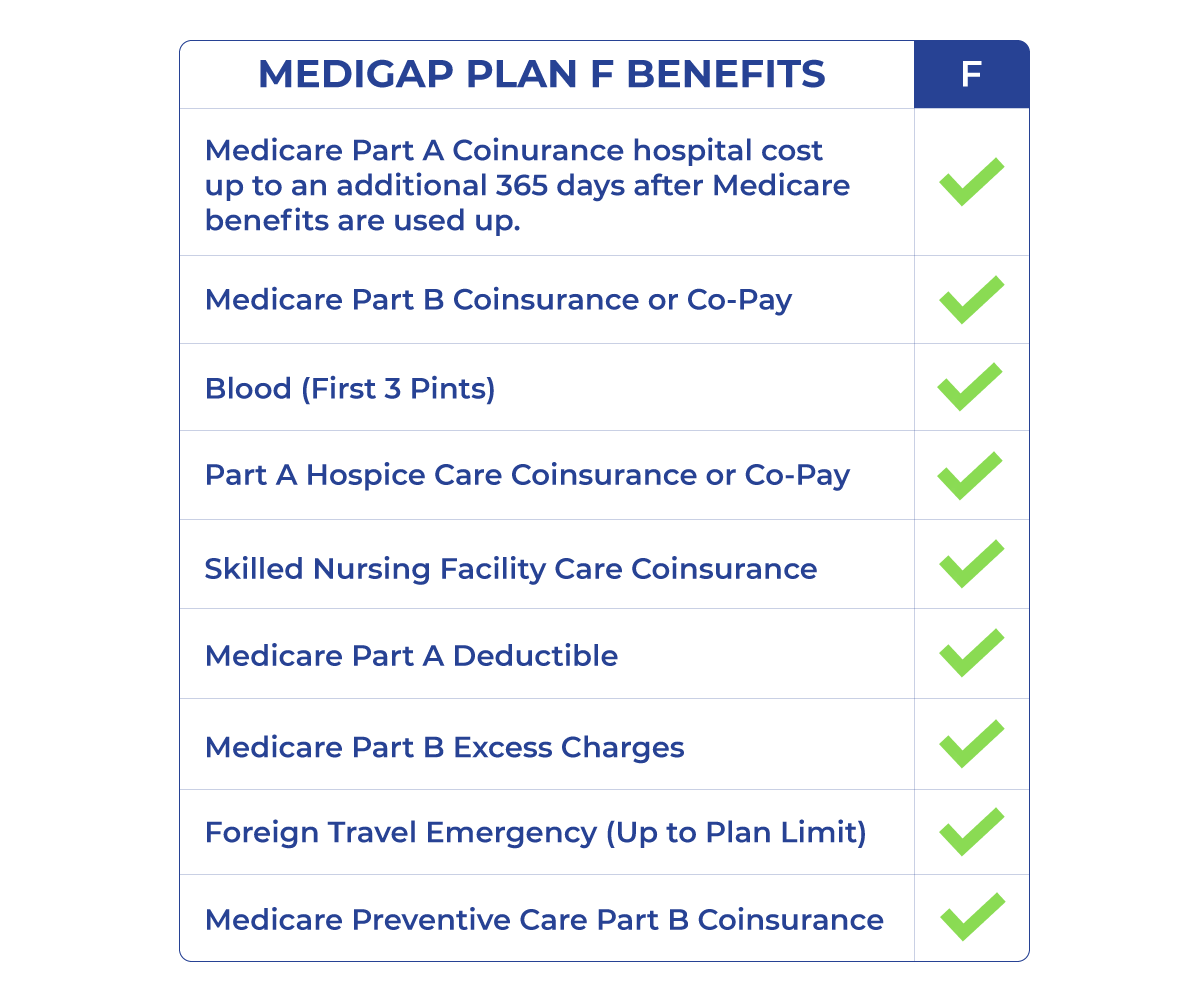

AARP Plan F provides coverage for Medicare Part A and Part B coinsurance, copayments, and deductibles, effectively shielding beneficiaries from many out-of-pocket costs. However, Plan F is typically more expensive than other Medicare Supplement plans due to its extensive coverage.

Let’s say John lives in California and has an AARP Plan F. He incurs a $1,000 hospital bill. Original Medicare covers a portion, leaving John with a $200 coinsurance. His Plan F would cover this $200, leaving John with no out-of-pocket expenses for the hospital stay.

While AARP Plan F is no longer available to new Medicare beneficiaries, those enrolled before January 1, 2020, can continue to benefit from its comprehensive coverage. The plan helps protect against high medical expenses, providing financial predictability and peace of mind.

Advantages and Disadvantages of AARP Plan F

| Advantages | Disadvantages |

|---|---|

| Comprehensive Coverage | Higher Premiums |

| Predictable Costs | Not Available to New Beneficiaries |

Frequently Asked Questions:

1. What does AARP Plan F cover? AARP Plan F covers Medicare Part A and Part B cost-sharing, including deductibles, coinsurance, and copayments.

2. Can I still enroll in AARP Plan F? If you were eligible for Medicare before January 1, 2020, you may still be able to enroll in Plan F. Otherwise, Plan G is a similar option.

3. How do I find AARP Plan F premiums in my state? Contact AARP or UnitedHealthcare directly, or use online comparison tools to get state-specific premium information.

4. Why are AARP Plan F premiums different across states? State regulations, healthcare costs, and competition among insurers all influence premium variations.

5. What is the difference between AARP Plan F and Plan G? Plan G is very similar to Plan F, but it does not cover the Part B deductible.

6. Is AARP Plan F worth the cost? This depends on individual health needs and financial situations. The comprehensive coverage provides peace of mind but comes at a higher premium.

7. What are alternatives to AARP Plan F? Other Medicare Supplement plans, such as Plan G, N, and D, offer different levels of coverage and cost.

8. How can I find the best AARP Plan F premiums? Compare quotes from different insurance companies offering Plan F in your state.

Navigating the intricacies of Medicare and its supplemental plans can be challenging. Understanding the nuances of AARP Plan F premiums by state empowers you to make informed decisions about your healthcare coverage. By carefully weighing your individual needs, exploring available options, and comparing premiums, you can secure the coverage that best aligns with your healthcare goals and budget. Remember to consult with a licensed insurance agent or utilize online comparison tools to gather personalized information and make the best decision for your future.

The allure of blue lined notebooks a deep dive

Tierno bebe kawaii imagenes de stitch exploring the cuteness overload

Is elvis presley still alive the enduring mystery

{kind=link}