Demystifying AARP Supplement Plan N Coverage

Navigating the maze of Medicare supplement plans can feel overwhelming. You're bombarded with letters, numbers, and options. One plan that often comes up in conversation is AARP's Supplement Plan N. But what exactly does AARP Supplement Plan N cover? It's a critical question to ask, and understanding the answer can significantly impact your healthcare expenses and peace of mind.

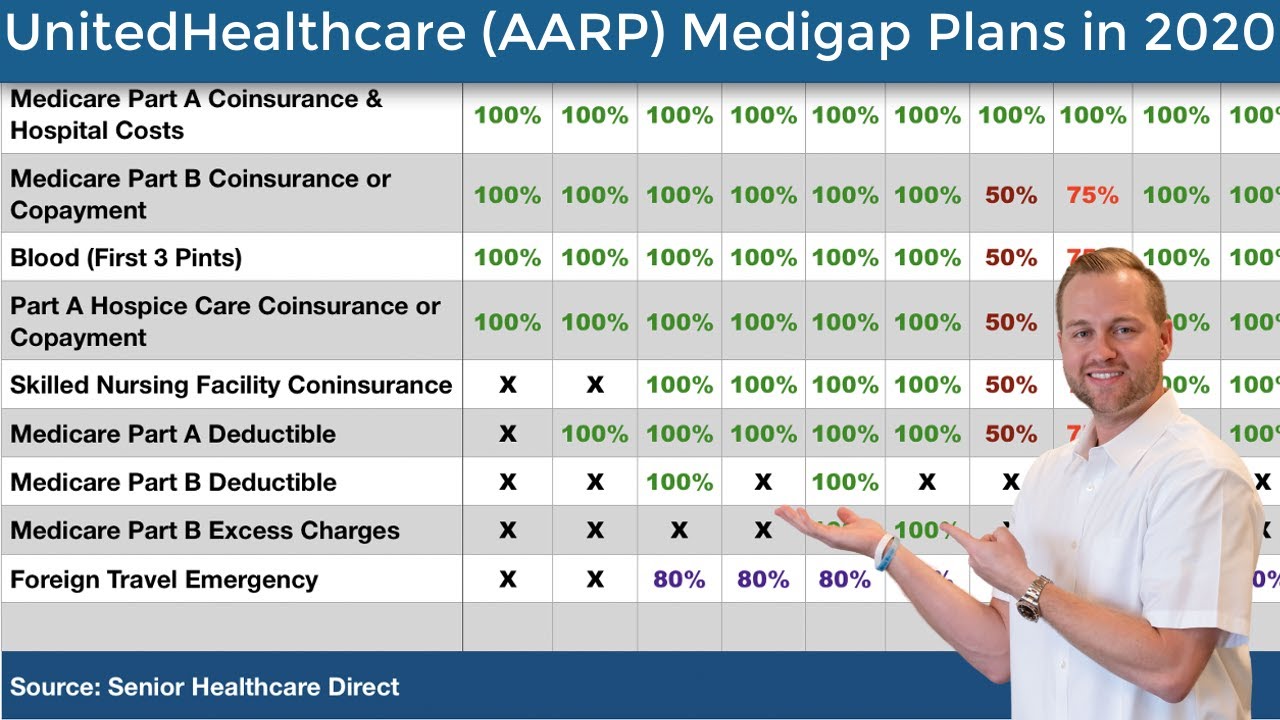

AARP, a well-known organization advocating for seniors, doesn't actually offer insurance plans directly. Instead, they endorse plans from UnitedHealthcare, a leading insurance provider. When people talk about "AARP Supplement Plan N," they're referring to UnitedHealthcare's Plan N, offered under the AARP brand. This plan is designed to fill the gaps in Original Medicare coverage (Parts A and B), helping to reduce your out-of-pocket costs.

So, what's the scoop on Plan N coverage? It picks up the tab for Part A coinsurance, Part B coinsurance (after you've met your deductible), and Part A hospice care coinsurance or copayment. It also covers the first three pints of blood you might need each year. However, Plan N doesn't cover the Part B deductible, and it has some cost-sharing features. You’ll be responsible for a copayment for doctor visits (up to $20) and emergency room visits (up to $50, unless you’re admitted to the hospital). Additionally, Plan N doesn't cover Part B excess charges.

Understanding these details is paramount when choosing a Medicare supplement plan. Do you anticipate frequent doctor visits? Are you comfortable with potential copayments? These are the types of questions you need to ask yourself. Comparing AARP/UnitedHealthcare's Plan N with other Medigap plans (like Plan G or Plan F) is also a smart move. Each plan offers different levels of coverage and cost-sharing, so finding the right fit for your individual needs and budget is essential.

Consider this: Mrs. Jones chose Plan N because she preferred lower monthly premiums and was generally healthy. The copayments for doctor visits didn't concern her. On the other hand, Mr. Smith opted for Plan G because he valued having all his out-of-pocket costs covered, even though it meant a higher premium. Their individual health situations and financial considerations guided their choices. Just like them, you need to weigh your own circumstances to make the best decision.

Advantages and Disadvantages of AARP Plan N

| Advantages | Disadvantages |

|---|---|

| Lower premiums compared to comprehensive plans like Plan G | Copays for doctor and emergency room visits |

| Good coverage for major medical expenses | Doesn't cover the Part B deductible |

| Offered by a reputable insurer (UnitedHealthcare) | Doesn't cover Part B excess charges |

One of the best practices for understanding AARP Plan N is to carefully review the plan's official documentation, available on the UnitedHealthcare website. Consult with a licensed insurance agent specializing in Medicare supplements. They can answer your specific questions and help you compare different plan options.

Frequently Asked Questions about AARP Plan N:

1. What does AARP Plan N cost? (Answer: Costs vary depending on location, age, and other factors.)

2. When can I enroll in AARP Plan N? (Answer: Typically, the best time is during your Medigap Open Enrollment Period.)

3. Can I be denied coverage for AARP Plan N? (Answer: Guaranteed issue rights apply during your Medigap Open Enrollment Period.)

4. Does AARP Plan N cover prescription drugs? (Answer: No, you'll need a separate Part D drug plan.)

5. Can I switch from Plan N to another plan later? (Answer: Yes, but you may have to undergo medical underwriting.)

6. Does Plan N cover skilled nursing facility care? (Answer: Yes, Plan N covers the Part A coinsurance for skilled nursing facility care.)

7. Does Plan N cover foreign travel emergencies? (Answer: Plan N provides some coverage for foreign travel emergencies, but it's limited.)

8. What is the difference between Plan N and Plan G? (Answer: Plan G covers the Part B deductible and excess charges, while Plan N does not. Plan N typically has lower premiums.)

Understanding the nuances of AARP Supplement Plan N is crucial for anyone considering this Medicare supplement option. This journey requires careful consideration of your individual health needs, financial situation, and preferences. Remember to compare Plan N with other Medigap plans, review official documentation, and consult with a licensed insurance agent. By taking these steps, you can empower yourself to make an informed decision that best safeguards your health and financial well-being. The right coverage can provide peace of mind, allowing you to focus on enjoying your retirement years rather than worrying about unexpected medical expenses. Take the time to research, ask questions, and choose wisely.

Decoding dosages your pocket guide to medication conversion chart printable

Decoding the kp group png logo a deep dive

Dirty flirty quotes for him

{kind=link}